Wiser Technology Advice Blog

- HOME

- WISER-TECHNOLOGY-ADVICE-BLOG

- IS BLOCKCHAIN THE ANSWER IT DEPENDS ON THE QUESTION

Is blockchain the answer?

20 March 2020

One of the latest ‘sexy’ trends in information technology is blockchain. There’s always of confusion and hype around any new trend, so I’d like to explain to you what blockchain actually is, when to use it, and when a ‘traditional’ system would more suitable.

In this blog post I'll cover:

- What is blockchain?

- How does blockchain technology work?

- What are private and public blockchains?

- How is blockchain technology being used?

- What are the downsides of blockchains?

- When is blockchain not the answer?

- Want to explore whether blockchain is right for you?

In last month’s blog I predicted a growing commercial use of blockchain technology platforms over the next decade.

I’ve attended three blockchain conferences over the last three years. The first of these in 2017 featured speakers who were explaining what blockchain is. in 2018 the conference speakers were exploring why and how to use blockchain technology, and an international blockchain summit, held in Adelaide Convention Centre in March 2019.

Blockchain is a difficult concept for people to wrap their brains around, but once it’s hidden away as an accepted underlying technology platform that won’t be an issue that end-users need to worry about.

What is blockchain?

Blockchain technology provides the ability to share transaction data without the need for a central authority such as a bank or share market. It removes unnecessary middlemen, allowing more efficient business processes and improving service delivery.

Blockchain was first invented as a platform for cyber currency Bitcoin, over ten years ago. In the last few years blockchain has come into broader use, particularly since the publicly available Ethereum blockchain platform was launched in 2014.

At the Information Technology in Aged Care (ITAC) conference in November 2018, one of the guest speakers was Rob Hanson, Senior Research Consultant, CSIRO’s Data 61.He provided a very succinct introduction to blockchain technology.

The first evidence of writing back in the mists of time was business and trading records created by accountants. Archaeologists discovered the earliest written records were ledgers of accounts engraved in stone.

For many hundreds of years ledgers were kept in carefully hand-written books, until the third industrial revolution in which computers were introduced. But ledgers maintained on these computer systems can have their records changed and altered without anyone noticing the changes.

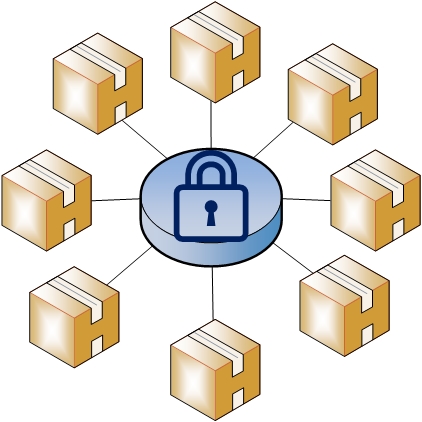

Blockchain is also referred to as Distributed Ledger Technology. In simple terms, the blockchain is just a chain of blocks of information from a ledger. However, each block of information, once created and saved in the chain, can never be changed or deleted. And the data is stored in computers distributed around the world, making sure it cannot be lost when a single computer fails.

So think of blockchain like a ledger which is tracking transactions in the cloud. The ledger spreadsheet is edited and locked, then linked to the next spreadsheet in the chain that is also locked. Everyone can see the transactions in the blockchain, but no-one can change or delete them.

How does blockchain technology work?

In simple terms, the steps for adding data into a blockchain are:

- 1.A new transaction is requested to be added to the blockchain.

- 2.The transaction is broadcast through the peer to peer network of computers.

- 3.Once verified as a from a trusted source, the transaction is combined with other transactions to create a new block of data for the ledger.

- 4.The new data block is made fixed and immutable, and permanently added to the block chain.

The outcome is a secure network of information, with blocks of data shared around computers on the network, secure and unchangeable. Blocks of data are never deleted from a public blockchain.

What are private and public blockchains?

The original blockchains set up for crypto currencies such as Bitcoin are public blockchains. These systems use anyone’s computer anywhere around the world as part of the system, running open source software to manage the blockchain in a distributed system.

Public blockchains are open to all, where no one is in charge. There is no access or rights management done for a public blockchain and anyone can opt in to be the part of the system. These blockchains are trustless, meaning there is no need for a trusted entity to overlook the operations as anyone in the blockchain can read, write or audit the public blockchain.

Private blockchains by contrast are controlled and managed by a central entity and you must have permission to join the blockchain and be able to read, write or audit transactions on the blockchain. In private blockchains, the owner of the blockchain is a single entity or an enterprise which can override/delete commands on a blockchain if needed. These are not truly decentralised, trustless systems so are more akin to a distributed ledger or database with cryptography to secure it than a public blockchain. Purists and pedants might question if private blockchains are actually blockchains in the true sense of the word!

Private blockchains are much less expensive to run in terms of energy consumption, so can provide a good optimised alternative for business systems. Private blockchain solutions allow multiple independent participants, for example companies in a supply chain, that need a central trusted source of truth for data to be shared by all.

How is blockchain technology being used?

The distributed ledgers of blockchain platforms have great potential to solve the problems of food security, by providing immutable proof of the provenance of food from the start of the supply chain to the consumer.

Blockchain can solve the problem of traceability of products, proving authenticity of products to consumers and tackling counterfeiting.

The wine industry of South Australia has taken up blockchain technology to prove the authenticity of wine sold to consumers overseas (particularly in China).

Data is collected each step along the way from harvesting grapes through to bottles of wine on shop shelves and data transactions are transmitted into a blockchain solution using internet of things devices such as RFID tags and QR codes.

This allows the people buying a bottle of wine a way to check each bottle’s authenticity, through scanning a QR code using their mobile phone.

A specific example of this blockchain solution idea was presented by the Clare Valley Wine and Grape Association at the 2019 ADC Blockchain Summit. Screw top wine bottles are commonly refilled with inferior wines and resold in China, which not only loses sales but damages the reputation of the winery and all Australian wines by association. This initiative proposes a QR code label be printed over the seal that is broken when a screw top is opened on a bottle. This QR code can be scanned by the consumer to access data stored on a blockchain that authenticates the provenance of the wine.

Thomas Foods International and Drakes Supermarket announced at the 2019 ADC Blockchain summit that they are launching an initiative that uses the IBM food trust blockchain. This is a private blockchain platform that’s already being used by Walmart in the USA. Drakes supermarkets would like all their suppliers to use this blockchain platform, as it will allow them to ensure the safety and traceability of food they sell to customers.

TravelbyBit is a travel booking platform that accepts Bitcoin as payment for travel bookings.

It aims to compete with other online booking platforms such as Expedia, with the difference of customers being able to pay for travel with crypto currency. Customers do not need to use a bank account or credit card to pay for travel, thus avoiding foreign currency exchange fees. TravelbyBit also offers a loyalty scheme, with those who use the booking platform earning Bitcoins as rewards.

This company already has 400 merchants using the booking platform around Australia, including 10 in South Australia. The main investor of TravelbyBit is Binance, a global cryptocurrency exchange.

What are the downsides of blockchains?

Public blockchains are self-governed and decentralised and have autonomy, because the method of decision making for what’s added to the blockchain is near impossible to tamper with. This has made blockchains the system of choice for criminal transactions on the dark web, as the data they hold cannot be seen by law enforcement agencies. For example, the Australian Computer Society has reported that $US 4 billion was laundered through cryptocurrency exchanges in 2019.

The autonomy of public blockchains may change in the future when Quantum computing power makes it possible to reverse engineer cryptography algorithms used in blockchains, but that’s many years away from reality.

Public blockchains consume an enormous amount of energy, particularly those which are used for mining of crypto currencies. The benefits of an autonomous, distributed systems require each node in the network be involved in processing every transaction, so large networks require huge amounts of power be constantly used, causing massive CO2 emissions from power generation. IT News reported that in late 2018 the Oak Ridge Institute for Science and Education found it takes more energy to process transactions on any of the four most popular cryptocurrencies (operating on blockchains) than it takes to mine actual metals like gold and copper.

Private blockchains are faster and cheaper by nature of being controlled by a single entity, so the enormous amounts of energy used in public blockchains are not required to reach consensus for each transaction on a private blockchain.

When is blockchain not the answer?

The chain is only as strong as its weakest link. The use case for blockchain to prove authenticity through a supply chain will only be successful if you can guarantee control over the entire supply chain. Every participant in the supply chain must agree to use Internet of Things devices to provide data to the blockchain to ensure an unbroken chain of information. The blockchain can be compromised with dodgy data if one of the participants in the supply chain cheats the system.

It does not make sense to use blockchain when a transactional system must process high volumes of data. The design of blockchain technology requires every node in the system be updated for every transaction, which requires a high amount of energy consumption, even in private blockchains. High energy consumption multiplied by high volumes of data transaction would make a distributed blockchain system enormously expensive to run and cause huge amounts of unnecessary CO2 emissions.

When all the data in a system must be owned by a central entity, a distributed blockchain system will not be the best solution. For example, a government agency that is the owner of data and provides information as a trusted source of truth would not allow external entities to have any way to create transactions in the system. This might be deployed as a decentralised system, using multiple data centres around the country, but all of the transactions in the system would be created only by the government agency.

Want to explore whether blockchain is right for you?

If you’d like to talk further about the possibilities of blockchain for your business initiative, get in contact with me today, I’m always happy to meet and have a chat over a coffee.

Further reading:

Thomas Foods International and Drakes Supermarket join IBM food trust blockchain. Available at https://www.supplychaindigital.com/technology/thomas-foods-international-and-drakes-supermarket-join-ibm-food-trust-blockchain

IBM food trust YouTube video. Available at https://youtu.be/QWijlTDHLMQ

Blockchain supply chain solution diagram provided by eBottli: https://www.ebottli.com

Australian Computer Society - $4b laundered through crypto exchanges in 2019. Available at https://ia.acs.org.au/content/ia/article/2020/-4b-laundered-through-crypto-exchanges-in-2019.html

IT News: Swinburne Uni tries to make blockchain practical for trade. Available at: https://www.itnews.com.au/news/swinburne-uni-tries-to-make-blockchain-practical-for-trade-537251

IT News: Mining Bitcoin now burns more energy than producing precious metals, including gold. Available at: https://www.itnews.com.au/news/mining-bitcoin-now-burns-more-energy-than-producing-precious-metals-including-gold-515111

CoinSutra: What are private blockchains and how are they different from public blockchains? Available at: https://coinsutra.com/private-blockchain-public-blockchain/

SmartDec: You do not need blockchain: eight popular use cases and why they do not work. Available at: https://blog.smartdec.net/you-do-not-need-blockchain-eight-popular-use-cases-and-why-they-do-not-work-f2ecc6cc2129